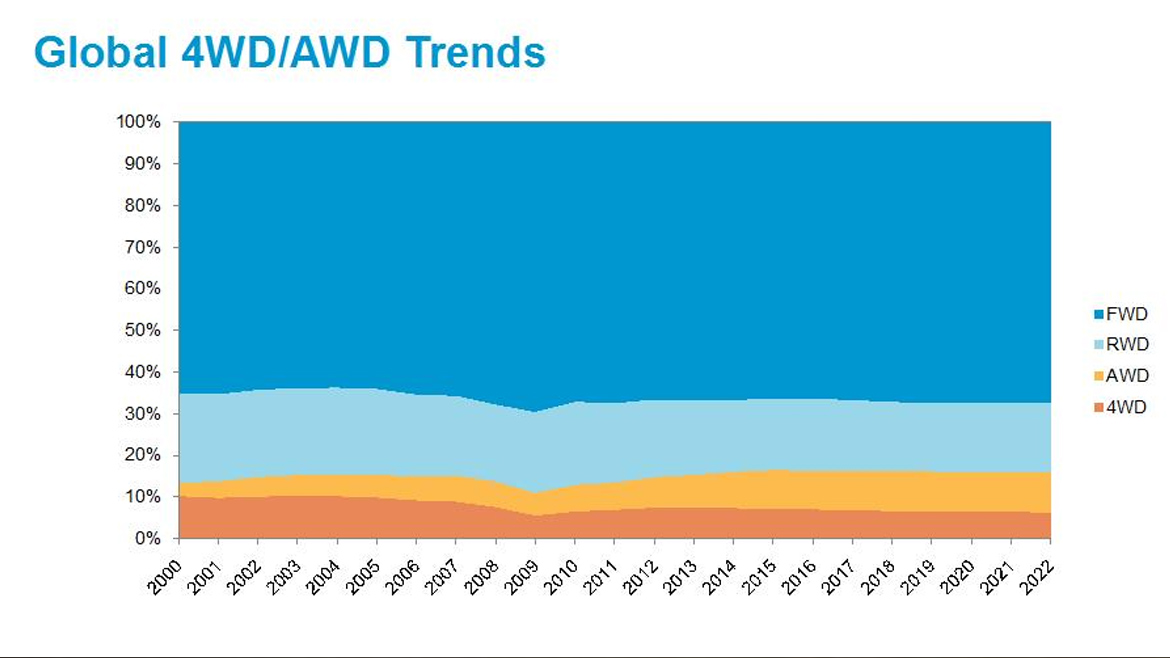

Yet for all the diversity of these individual regional trends, the aggregate global share for each of the principal drive configurations will remain broadly unchanged from today’s values. By 2022, according to data analysts IHS, global aggregate demand for FWD models will be little changed from today’s dominant value of around 45 percent; the next most popular architecture, and again substantially unchanged, will be rear-wheel drive (RWD) at some 15 percent. AWD systems will gain in share slightly against the less-sophisticated 4WD set-up; together, they will account for almost 20 percent of global drivetrain production.

In compiling his presentation for the European All-Wheel Drive Congress in Graz, Austria in April this year, IHS manager of EMEA powertrain forecasting Chris Guile defines AWD vehicles as models based on a FWD platform, while 4WD refers to vehicles derived from RWD architectures.

Analyzing the trends, Guile observes that, although the production penetration of the different architecture types will remain relatively constant, differing growth rates in each region will mean much sharper differences in numerical production volumes. Numbers are expected to remain static in the Middle East, Africa and South America, but increase slightly in South Asia. Most of the volume boost will be accounted for by greater China, Europe and, especially, North America, where 4WD/AWD penetration will peak at almost 35 percent before leveling off by 2022.

IHS’s forecasts are based on confidential model and planned production information supplied directly by the OEMs themselves, and give an accurate picture of aggregate manufacturing volumes and splits for the upcoming generations of models hitting the showrooms in the years up to 2022.

Manufacturer trends

Equally intriguing is the forecast evolution in 4WD/AWD production share for individual marques. Land Rover, which was 100 percent 4WD for the first half-century of its history, only began to introduce a lower-cost FWD option on its Freelander leisure SUV in 2011, and now the spectacular success of the smaller and predominantly FWD Range Rover Evoque has pulled the brand’s 4WD/AWD penetration down to around 95 percent. Further inroads of smaller and lighter Land Rover and Range Rover leisure SUVs will take the brand to below 90 percent AWD by 2022, says IHS.

Surprisingly, well before this decade is out Land Rover will have lost its traditional position as the major automaker with the highest share of 4WD/AWD production. The interloper is Subaru, which will see rising volumes of its high-performance sedans and crossovers in relation to its simpler minicars and kei-cars. Traditional 4WD specialist Jeep, meanwhile, will see its AWD penetration slip to some 65 percent as it grows its share of smaller Fiat-based compact crossovers, many of which are preferred by customers as FWD models without the additional drive option.

German premium majors Audi, BMW and Mercedes-Benz will continue to boost their AWD/4WD penetration, with Audi increasing its advantage so that by 2019 every second Audi will be a quattro® model with all four wheels driven. By contrast, volume producers such as Ford, Nissan, Toyota and Honda will steadily lose AWD penetration as the perceived cost and fuel consumption penalties deter cost-conscious customers and improved FWD traction control systems reduce the likely advantage of AWD in winter conditions.

Sector trends

While the global market for light pickups up to 6 tons GVW will remain overwhelmingly RWD and 4WD, by 2022 a growing fraction will be front-driven and a limited number of AWD models will also appear. Among SUVs, the big trend will be a large jump in volumes from 18 m units today to some 28 m by 2020. The principal growth, say the IHS charts, will be in FWD platforms and their AWD spin-offs. B-segment SUVs, overwhelmingly front-driven, will fuel the bulk of this rise.

The mainly premium D and E segment will remain faithful to RWD, but the proportion of purely FWD cars will reduce as these models begin to offer AWD derivatives. Hybrids, which IHS forecasts will enjoy a 10 percent share of global light vehicle production by the end of the survey period, will contribute to the AWD/4WD share as designers add supplementary electric drives to the secondary axle. Guile questions whether BMW and Mercedes-Benz will bring hybrid capabilities to their generally smaller FWD models by the addition of an electric rear axle; the alternative would be an e-motor built into the standard front-drive transmission.

Electric vehicles, finally, are forecast to remain below 1 percent global market share by 2022, with the overwhelming majority two-wheel drive. Exceptions, says Guile, will be pricey models such as the Tesla, Audi R8 eTron and Mercedes SLS/GT. Intriguingly, Guile also points to the unconfirmed possibility of AWD EVs from Land Rover, Chevrolet (Volt) and the soon-to-appear fourth-generation Toyota Prius.

Overall, concludes Guile, the 4WD/AWD market will remain globally stable but with differing OEM and regional trends, and penetration rates will tell a different story than absolute volumes. Finally, EVs do not, in IHS’s view, pose a major threat.